Issue4: Material Efficiency - Recycling

ConsultationPaper on Recovery and Recycling Targets for Packaging Waste in 2001

The purpose of this corporate submission is to re-emphasize thefollowing 5 points of strategic significance from which we never deviated since1994.

I We would point out that the waste industry was specifically excluded fromthe very first discussions with Sir Peter Parkers group in the context ofthese Packaging Regulations and in consequence the framework was flawed from thestart due to the fudge of shared responsibility and the dislocation ofliability and rewards between the various parties.

II Our assertionflawed is based on the fact that the financial benefits accruing out of theProducer Responsibility Note system (which was not originally envisaged when theRegulations were drawn up) flows to the reprocessors. This demand pull assumption has been demonstrated to be anunrealistic one. The system shouldbe constructed on the basis of supply push. Tradeable Permits regime should reward those who physically separate andrecover material and make it available through the waste industry forreprocessing.

III Supply push scenariosare intrinsically more efficient because:

(i) Packaging users in the supply chain have aninbuilt incentive to segregate scrap material for recycling because of therewards especially if Landfill Taxes are increased to European levels.

(ii) Users have an inbuilt incentive to register to access Tradeable Permitsobviating the current problems with free riders.

(iii) Random checks on an exception basis can be more cost effectivelyorganised via the Environment Agency or compliance scheme if an integratedreporting framework is agreed with the waste and reprocessing sectors.

(iv) Thereare inbuilt incentives to maintain accurate input data because it determines thecorporate qualification for Tradeable Permits.

(v) This system generatessurplus supplies of recovered material which will drive down gate fees forrecovered product.

IV There is as much logic inallowing incineration plants to issue PRNs for packaging flow inputs as therewould be to give the same facility to landfill operators. If incineration plants continue to receive funding flows from PRNs thenan incineration tax should be levied which matches this income benefit.

V If the supplypush option is rejected demand pull should be operated in its simple most effective format by dispersing with the fudge of shared responsibility. Single point responsibility is needed probably at the reprocessorstage.

The current compromise merely results in around 80m per annum beingtransferred from all supply chains to material reprocessors/manufacturers.

Two more important initiatives must be developed with some urgency:

(a) A high level round-table focussed on developing a framework UK strategyon Tradeable Permits involving the DTI/Treasury/DETR/CBI/LGA.

(b) A specialist waste subgroupcharged with examining (on an interim basis) the data management, logistics,pricing transparency and investment implications of the existing framework forTradeable Permits on scrap materials.

British industry will be handicapped by operating with a series of halfbaked, economically illiterate ad hoc Tradeable Permit systems which varyaccording to product, supply chain structure or the view of the governmentdepartment responsible for implementation. Free market systems will be distorted, middlemen will create speculativebubbles and improved resource efficiency will be subsumed in a welter ofartificially concocted and contradictory market instruments.

PolicyInstruments to Correct Market Failure in the Demand for Secondary Materials

It is also important to eliminate the dysfunctionality in policy makingoriginating in Government which - in the environmental area - is in danger ofexposing key industry sectors to death by a thousand cuts.

(i) The use ofexternality fiscal instruments on an across the board basis regardless ofmaterial or industry sector should be resisted at all costs because it is likelyto be too blunt and:

too rigid and unresponsive,

in danger of having an incorrectly developed theoretical base,

it may produce significant disincentives to inward investment andUK employment prospects if we act singly on a national basis,

it may be difficult to reward improvements over time in specificsectors,

it may be difficult to recognise intra sectoral best practiceoperations on a company by company basis.

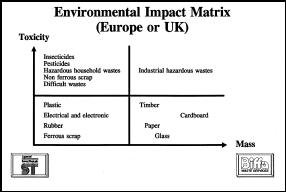

(ii) We believe thatcharge-subsidies mechanisms are of primary relevance tohigh mass low toxicity sectors. Thefollowing matrix is an approximation of material streams appropriate to thissort of analysis.

TheTreasury have already indicated that any net income streams arising from the useof economic and financial instruments are netted off through lower NationalInsurance Contributions (NICs). Subsequentevents have demonstrated the dangerous downside impacts associated with crosssectoral benefits. The matrixdemonstrates the potential for transfer impacts between sectors which areexposed to environmental taxation processes.

|

|

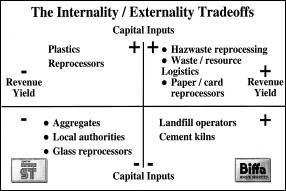

(iii) We would suggest that thefollowing matrix could be a starting point (offsetting companies with highinternality environmental costs to themselves against companies/productsectors which produce high externality costs for their customers and society atlarge).

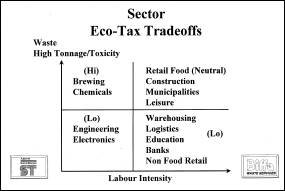

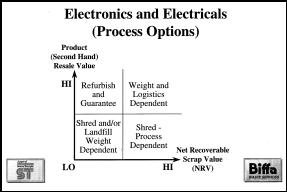

(iv) priorities for actionmight be defined sector by sector and then there is scope for identifying the intrasectoral product initiative priorities. Using the example of the electrical and electronic sector for instance itmight be possible to identify where zero externality fiscal instruments arerequired simply because the perceived reclaim value of the material more thanoffsets the potential cost reclaim. Thefollowing matrix offers some suggestions on this point:

(i) Whatis missing is a more holistic understanding of the key overarching integrationrequired between economic, financial and regulatory instruments. Producer Responsibility and Integrated Product Policy (IPP) are essentialand in the long run will be far less costly and less complex to operate.

(ii) Thesecond overarching principle should be that any sector accepting life longliability for their product should (as a quid pro quo) operate within aframework of cost neutrality. Itis thus necessary for industry and Government to develop voluntary frameworkagreements whereby transition costs involved in transferring externalities intointernalities is a phase in process over an agreed number of years - but notexceeding 6 - or 8.

(iii) Thethird overarching principle we would like to seeis a significant emphasis on data and audit systems.

(iv)

(a) ProducerResponsibility and voluntary agreements in preference to detailed marketinstruments.

Thismechanism will produce a dramatic improvement in sustainability decision makingand end market recyclate reuse for the following reasons:

There is a linkage betweenthe authority to pollute and the responsibility for pollution minimisation.

Those pressures usually manifest themselves in terms of:

Reduction in the toxicity/dose content of their products.

Weight minimisation.

The development of sophisticated data capture systems with respectto life cycle product flows.

The creation of innovative lease/take back arrangements.

A re-assessment of primary manufacturing technologies.

A re-assessment of in life pollution potential.

Producer Responsibility mechanisms lead to the development ofpotential large scale, strategic and high route density cost effective logisticsreclamation systems.

Such systems lead to the emergence of accessible consumerinformation systems.

There tends to be more focused product centred leadership inrelation to local authorities.

In response to the above transfers of cost liability from localauthorities to producers there could be abenefit to the Exchequer of up to 500m per annum in the form of reduced localauthority waste management costs.

Producer Responsibility accelerates strategic partnerships betweencapital goods suppliers and consumable material suppliers.

(b) Offsettingthe cost of Producer Responsibility.

Transparentaccounting processes independently overseen by a Government body are essentialto this process. Tenders should belet competitively and advertised on a regional basis in conjunction with theRegional Development Agencies. TheEnvironmental Audit Select Committee of the House of Commons has alreadysuggested that a Green Tax Commission (GTC) be formed and it would be rationalto integrate the overview responsibility of any PRG schemes under that umbrella,with input from the Office of Fair Trading.

Our researchidentifying hypothetical all in collection and reclamation costs for materialstreams originating in different product areas suggest that these will often bein the range of 1%-3% of top line sales.

|

|

1%-3% onsales turnover may not sound much but it is often equivalent to the PBIT of theentire supply chain. How are theseincremental costs to be offset?

(c) Incremental revenuecosts.

Implicit in the process is a proposal that PRGs should apply to an offset fund created from net proceeds of Landfill Tax. In our response to the National Waste Strategy we suggest that in year one PRGs should be funded up to the amount of their openly tendered and bid contracts for material reclamation but then the PRG should agree with the regulator (OFFWASTE?) a time period over which such support moves down to zero. In this way externality costs are transferred onto the producer and the initial kick-start funding becomes self liquidating within a foreseeable time frame, with retail prices rising pari passu.

We believe parallel drivers (in the form of grants of around 10 per household to local authorities) funded from net proceeds of the Landfill Tax, could kick-start a substantial range of kerbside schemes.

Tradeable Permit systems should receive greater emphasis as an incentive.

Implicit in any voluntary agreements reached by PRG/industry sectorbodies is an element for replacement of capital infrastructure. Sectors such as newsprint lack the profitability base to exercise largescale capital write-off on plant which currently runs on virgin input materialand may need to be scrapped in favour of new capital capable of acceptingsecondary and recovered raw material. Thesecapital 0n-costs need to be considered as part of the kick-start offset process.

We propose the development of an OFFWASTE equivalent operating inclose coordination/ direct subordinate role to the proposed Green TaxCommission. Such a body should havethe same regulatory and legislative influence of other utility regulatorsalthough their position vis--vis the Environment Agency may requireexamination.

We sincerely believe the measures outlined above will contribute substantiallyto correcting existing market failures.

To consider material stream fiscal instruments whilst ignoring the macroeconomic framework of existing Government strategies is potentially dangerous. Conflicting policy instruments - whether fiscal, budgetary, economic orregulatory send conflicting messages into the same sector.

Government should accept a light hand on the tiller approach with resortto the mailed fist (by mailed fist we mean resort to more fundamental measuressuch as outright landfill bans or the threat of virgin input resource taxes)when it becomes apparent that interim or final targets are unlikely to be met. Such an approach carries significant advantages in:

(i) a reduction ofregulation,

(ii) a reduction in the cost topublic funds of waste disposal and administration,

(iii) a more strategic role for theregulator.

The contents of the site are protected under copyright - Biffa Waste Service Ltd 2001 No reproduction is permitted without prior permission