Exhibit 1

Exhibit 2

Issue5: Biodiversity - Sustainbility

The Biffaward Approach to Strategic Sustainable WasteManagement Initiatives by the Application of Landfill Tax Funding

In 2004 it is vitally importantto have evidence of strategic initiatives underway or completed for whichgenuine claims can be made that the work would not otherwise have beenundertaken.

It is commonly acknowledged that there is a dearth of sound data onwhich to develop effective sustainability strategies. Our mould breaking publication - "Great Britain plc: TheEnvironmental Balance Sheet" - was designed to highlight thoseshortcomings.

In consequence we are seeking toreserve a significant proportion of our funding flows for applications whichfocus on the sectoral opportunities for sustainable waste managementenhancements driven by improved awareness of their existing resource flowsthroughout the supply chain. Suchinitiatives are founded on the following core assumptions:

(i) Few industry sectors possess a holistic understanding of their relianceon landfill as a percentage of their overall end of pipe waste arisings.

(ii) Industry sectoral overviews can be developed on how mass andtoxicity can impact on product redesign.

(iii) Suchanalysis also accelerates understanding in the sector with regard to thedirection/scale and impact of forthcoming regulatory, fiscal and budgetaryinstruments.

We seek to expand the logic ofdeveloping mass balance flow research studies for 3 distinct:

(i) In an industry sectordimension.

(ii) In a material streamdimension.

(iii) In a geographic dimension.

What is the Objective?

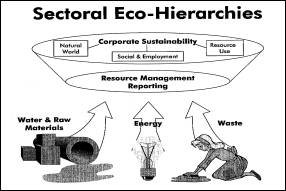

Mass balance flows relate notonly to the input of raw materials but to the total environmental impactof the sector - embracing solid, gaseous and liquid resource inputs and outputs. Thereby an understanding of the (usually) overwhelming significance ofsolid waste arisings is put into context.

The intention is to develop aframework reference document and web site identifying the risks, costs andpitfalls associated with various technology shifts which could contribute tochanges in end of pipe waste streams.

What is The Relevance of This Approach to The Sustainable WasteManagement Strategy?

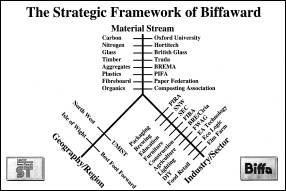

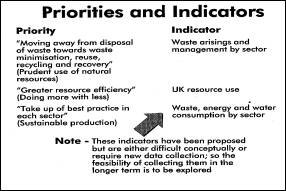

Government initiatives focus on theprudent use of national resources. Exhibit3 summarises these initiatives in precise form and exhibit 4 is a direct quote.

|

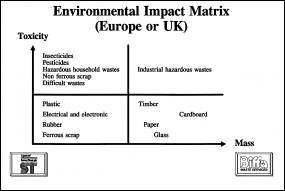

Exhibit 1

|

Exhibit 2 |

|

|

|

|

Exhibit 3

|

Exhibit 4 |

|

|

Our objective is to alertindustry sectors to the collective material flows of their sector to landfilland place these in the context of their overall operational resource impactsthroughout the entire supply chain.

Our intention is to encourage amore strategic overview of the environmental management shifts needed in theirsupply chain, marketing and sourcing strategies.

What is The Nature of Deliverables From The Projects?

The end deliverables will takethe form of a written publication and web site.

In addition it is proposed thateach package will contain around 15k-20k of support for quality controlledteachers to be seconded to the project.

Funding Flows

Biffa have earmarked between 120k and 150k for each scheme and ourexpectation is that the gross spend over the period 1999-2004 could amount toaround 10m-12m.

Other Biffa Strategic Initiatives

in the social and naturaldimensions we are funding strategic initiatives. The most notable examples of these are a mass balancesustainability survey for North West England, the 900k - 3 year - ottersproject and a 1m schools education project with Going for Green.

Conclusion

We believe a significant gap exists in the pool of informationavailable to Government, NGOs, trade associations and the general public withregard to mass balance resource flows. Inthe absence of any proactive Government strategy to develop that understandingthere is a clear opportunity for Landfill Tax schemes to service thisinformation gap.

AppendixI

SkeletonFramework for an Industry

SectoralMass Balance Study

I Introduction/ExecutiveBrief

Synopsis of the sector pressures from an environmentviewpoint.

Key drivers for change in the dimension of economic, social andnatural issues.

Wish list of target environmental position in 10, 20, 30years.

Threats and blockage points.

Objective of study/feedback mechanisms.

Key conclusions.

II Facts and Figures

Inputs analysed by:

material types (a)

geography of origin/use (b)

imported/home produced/sources (c)

seasonality (d)

method/technology (e)

tonnages (f)

key players/actors (g)

Conversion/manufacture - by all of the above

Sale/distribution - by all of the above

End life receptors - by all of the above

III The Historical and CurrentContext (the context of the mass flow)

Past trends of use/consumption, etc

How the sector/stream evolved environmentally

Technology shapers to the process

Background to location/logistics/infrastructure patterns

Turnover/capital employed/profits pattern

Market drivers in the past

Raw material patterns/supply chain infrastructure

Fiscal/budgetary instruments (existing and forecast)

Corporate ownership patterns (level of market concentrationintegration)

Integrated Product Policy (IPP) impacts/Producer Responsibility

Product (as opposed to resource) flows

IV Future Trends and Pressuresfor Change

A

Market drivers (product mix, composition, performance)

Pollution load/regulatory drivers (especially landfill diversionimpacts) to other sectors and uses

Technological drivers/innovation

Supply chain issues (SMEs/raw materials)

Natural world/ecological drivers (species/habitat issues)

Political issues (planning, regions/LAs/trade/regulation)

B

Synopsis of high/medium/low sustainability indicators for 5, 10,20 year outlook in the context of DETR indicators. Are there any? What should they be? (Focuson material balance of the future - compare and contrast to 1999).

C

Gaps/shortfalls/blockages:

research?

academia?

social issues/employment impacts?

ethical issues?

Government initiatives?

Tradeable Permit regimes?

V Glossary of Terms

VI Detailed Bibliography

Note- Vignette Data

Using Great Britain plc asa template, insert boxes can contain storylines on key issues, specialistprocesses, subset data, examples, real life cases, academic studies, etc tospice up the layout.

Literary style should be focusedon the man and woman on the Clapham omnibus, regulators, MPs, civilservants, customers, trade association, teachers - in fact, everybody!

Appendix II

SkeletonFramework for a Material Stream

SectoralMass Balance Study

I Introduction/ExecutiveBrief

Synopsis of the material stream pressures from anenvironment viewpoint.

Key drivers for change in the dimension of economic, social andnatural issues.

Wish list of target environmental position in 10, 20, 30years.

Threats and blockage points.

Objective of study/feedback mechanisms.

Key conclusions.

II Facts and Figures

Inputs analysed by:

material types (a)

geography of origin/use (b)

imported/home produced/sources (c)

seasonality (d)

method/technology (e)

tonnages (f)

key players/actors (g)

Material conversion/manufacture - by all of the above

Material sale/distribution - by all of the above

Material end life receptors - by all of the above

III The Historical and CurrentContext (the context of the mass flow)

Past trends of use/consumption, etc

How the material/stream evolved environmentally

Technology shapers to material use

Background to location/logistics/infrastructure patterns

Turnover/capital employed/profits pattern of users

Market drivers in the past

Raw material patterns/supply chain infrastructure

Fiscal/budgetary instruments (existing and forecast)

Corporate ownership patterns (level of market concentrationintegration)

Integrated Product Policy (IPP) impacts/Producer Responsibility

Product (as opposed to resource) flows

IV Future Trends and Pressuresfor Change

A

Market drivers (product mix, composition, performance)

Pollution load/regulatory drivers (especially landfill diversionimpacts) to other sectors and uses

Technological drivers/innovation

Supply chain issues (SMEs/raw materials)

Natural world/ecological drivers (species/habitat issues)

Political issues (planning, regions/LAs/trade/regulation)

B

Synopsis of high/medium/low sustainability indicators for 5, 10,20 year outlook in the context of DETR indicators. Are there any? What should they be? (Focus on material balance of the future - compare andcontrast to 1999).

C

Gaps/shortfalls/blockages:

research?

academia?

social issues/employment impacts?

ethical issues?

Government initiatives?

Tradeable Permit regimes?

V Glossary of Terms

VI Detailed Bibliography

Note - Vignette Data

Using Great Britain plc asa template, insert boxes can contain storylines on key issues, specialistprocesses, subset data, examples, real life cases, academic studies, etc tospice up the layout.

Literary style should be focused on the man and woman on the Claphamomnibus, regulators, MPs, civil servants, customers, trade association,teachers - in fact, everybody!

Pre-Budget Report 1999: Taxes on Pesticides & Aggregates and the Climate ChangeLevy

(i) We suggest that externally imposed financial instruments are lessadaptable, flexible and market sensitive as mechanisms likely to flow fromvoluntary schemes operating in specified product sectors. Producer Responsibility, backed by targets, voluntarily agreed TradeablePermit systems and fully transparent data collection systems, offer a preferableroute to sustainability in tune with market realities.

(ii) It is important to eliminate the dysfunctionality in policy makingoriginating in Government which - in the environmental area - is in danger ofexposing key industry sectors to death by a thousand cuts.

(i) The use of externality fiscal instruments on an across the board basisfor all materials should be resisted because such an approach tends to be:

too rigid and unresponsive,

in danger of having an incorrectly developed theoretical base,

capable of producing significantdisincentives to inward investment

difficult to reward improvements over time in specific sectors,

difficult to recognise intra sectoral best practice operations ona company by company basis.

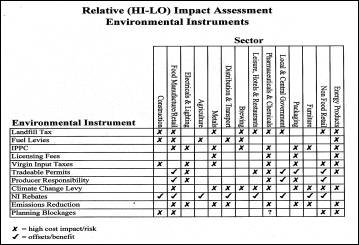

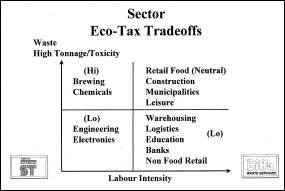

(ii) The Treasury have already indicated that any net income streams arisingfrom the use of economic and financial instruments are netted off through lowerNational Insurance Contributions (NICs). Subsequentevents have demonstrated the dangerous downside impacts associated with risks ofcross sectoral transfers. Thematrix demonstrates the potential for transfer impacts between sectors.

(i) What is required is a more holistic understanding of the integrationrequired between economic, financial and regulatory instruments inthe context of Government strategy. Webelieve that Producer Responsibility and Integrated Product Policy (IPP) areessential and in the long run will be far less costly and less complex tooperate as a concept when compared to an intricate framework of fiscal burdens. The latter will distort free market economics in what isincreasingly becoming a global market for global chemical companies.

(ii) Producer Responsibility, however, carries with it incremental costs tothe sector. Anysector accepting life long liability for their product and the associated costsof end life neutralisation should (as a quid pro quo) operate within a frameworkof cost neutrality (at least in yearone). It is thus necessary forindustry and Government to develop voluntary framework agreements wherebytransition costs involved in transferring externalities into internalities is aphase in process over an agreed number of years - but not exceeding 6 - or 8.

(iii) We would like to see a significantemphasis on data and audit systems to reassure Government, regulators andthe Office of Fair Trading that this internalisation of externalities process isnot occurring at the expense of market distortion, exercise of unfair marketpower or lack of equity in relation to the market strength of existing sectoralplayers.

The contents of the site are protected under copyright - Biffa Waste Service Ltd 2001 No reproduction is permitted without prior permission